Everything is bank.

How many apps are holding your money right now?

Recently, my showerhead split open, spewing water in every direction, and so for a week, my sister and I would shower under a single jetstream of water that shot out from a pipe in the wall, which seemed to get more and more powerful every time I used it. So we took to Amazon to buy a new one.

We scrolled through 10,000+ near-identical chrome fixtures to land on the $45 masterpiece that is now affixed to the pipe in our shower — but what piqued my interest was what happened at checkout.

Before you can click “buy”, Amazon offered me: an Amazon Prime Visa (5% back), an Amazon Store Card (0% APR financing — for a showerhead), the option to pay in installments through Affirm, or to reload my Amazon gift card balance. Four separate financial products.

This wasn’t always how buying things worked. Banks used to be imposing marble institutions you visited with trepidation to access your money. Now the companies engineered to make you spend money are managing it.

Starbucks holds more customer deposits than many regional banks. Airlines have become credit card companies that fly planes on the side. Your grocery store, your coffee shop, that online clothing company, your social media platforms — they’re all banks now, or something close enough.

When the same company that’s trying to sell you things is also holding your money, offering you credit, and managing your rewards points as private currency, something fundamental changes about how we perceive and behave with money itself.

The infrastructure that made this possible

In 2020, the venture capital firm Andreessen Horowitz published a piece called “Every Company Will Be a Fintech Company,” arguing that there was a market incentive for almost any company to offer financial services, since the margins were so good.

Silicon Valley gave this a name: “embedded finance.” Also known as: bankification.

They were right. The global embedded finance market was valued at $104.8 billion in 2024 and is projected to grow at 23.3% annually through 2034.

Banking-as-a-Service platforms mean companies don’t need to become actual banks with all the regulatory burden that entails. Instead, they partner with a licensed bank on the backend — the bank handles compliance and holds the official accounts — while the company controls the customer-facing experience and captures a large part of the economic value.

Many companies already process payments. They already have your transaction data. They already know your spending patterns and behavioral triggers. They’re just one step away from offering accounts, cards, or loans.

And the profit margins are obscene. For large retailers, store credit cards generate up to 14% of total company profits. Payment processing generates billions — Visa and Mastercard collect 2-3% on every transaction, and companies that bring these services in-house capture that spread. Starbucks earned an estimated $150-200 million annually just from interest on customer balances before interest rates dropped.

Target’s RedCard drives 20% of sales. Walmart’s financial services division generates over $1 billion annually. More than half of major banks now earn over 51% of their revenue from embedded finance partnerships with fintechs and non-financial companies. The traditional banking system isn’t fighting this — they’re enabling it as white-label infrastructure providers.

The companies get four things from this model:

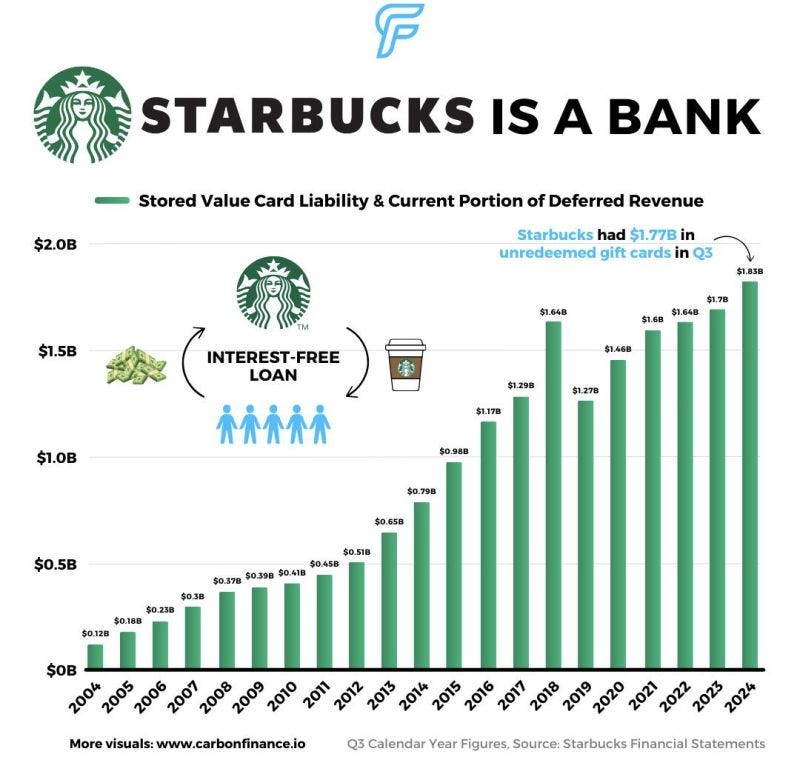

Interest-free capital: Your preloaded balances and gift cards are money they can use immediately. Starbucks holds nearly $2 billion in customer deposits — essentially an interest-free loan from millions of customers.

Forgotten money: In 2023, Starbucks recognized $215 million in “breakage” — forgotten balances that legally convert to company revenue after a certain period. A study by Bankrate found that 43% of people have unused gift cards, with an average value of $244 per person.

Surveillance data: Every transaction reveals behavioral patterns worth far more than the transaction itself. They’re not just seeing what you buy — they’re tracking when you buy (paycheck cycles, stress purchases, time of day), what prompts you to spend (emails, push notifications, location triggers), and what price points make you convert. This data gets fed into algorithms that learn your personal spending ceiling. Companies monetize this data: selling anonymized purchase data to brokers, using it to optimize exactly which offers to show you, learning precisely how much friction to remove before you spend.

Customer lock-in: Once your money and payment history live in their ecosystem, leaving becomes incredibly costly and a high effort to move.

This creates a perfect storm: they’re holding your money, studying your behavior, and using that information to extract more money from you. The same company that knows you’re financially stressed (because they can see your purchase patterns) is the one offering you credit.

From deposits to surveillance pricing

The companies holding your deposits are the same ones using your data to charge you more.

Last October, The Washington Post investigated Starbucks Rewards and found something quite disturbing: the company was tracking every purchase from its 34 million rewards members, then using that data to give fewer deals to their most loyal customers.

In other words, the more frequently you bought from Starbucks, the fewer promotions you received. The algorithm determined you’d buy either way, so why offer you a discount?

This is surveillance pricing: Using detailed behavioral data to figure out exactly how much each person is willing to pay, then charging them accordingly. Most companies don’t create loyalty programs out of the goodness of their hearts. Many use them to extract more data from you, to study you.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

A recent report from Vanderbilt found that loyalty programs have “evolved into data-harvesting machines” that track not just purchases, but who you are, what you search for, how you move your cursor across a screen. The coffee is almost beside the point. The real product is you — and the financial infrastructure to hold your money while learning exactly how much more they can extract.

This has wider economic implications. Per this article from Jacobin,

“Financial policy watchdogs warn that bankification is unleashing predatory and fraudulent practices onto consumers, workers and smaller businesses. It may even lay the groundwork for the next financial collapse. After all, can a widget factory be trusted to manage customers’ money and make safe lending decisions without putting the entire financial system at risk?”

While all of this has been happening, the regulatory infrastructure meant to prevent it has been systematically dismantled.

The Trump administration reopened applications for industrial loan companies — the auto-industry banks whose risky lending practices helped fuel the 2008 financial crisis. These are corporate-owned banks that can make loans and take deposits without the full regulatory oversight of traditional banks.

The CFPB, which was created specifically to prevent this kind of predatory financial service, has been under constant attack. The agency proposed rules in 2024 that would bring major payment apps like Apple Pay, Google Pay, and Venmo under the same oversight as banks — but tech companies have fought back hard, and the political will to enforce these rules remains unclear.

Former CFPB official Amanda Fischer put it plainly: “It’s a really good way to take the U.S. government hostage.” If Apple Pay or Amazon banking fails with millions of people holding balances, that becomes a taxpayer bailout situation. In some ways, we learned nothing from 2008.

When airlines become credit card companies

Delta Air Lines is technically an airline — it still flies planes and everything. But in the third quarter of 2025, Delta received approximately $2 billion from American Express, representing a 12% increase from the same period the year before. For the full year 2024, Delta earned about $7.4 billion from its Amex partnership.

That’s nearly equal to the amount Delta generated from actually flying passengers in 2022.

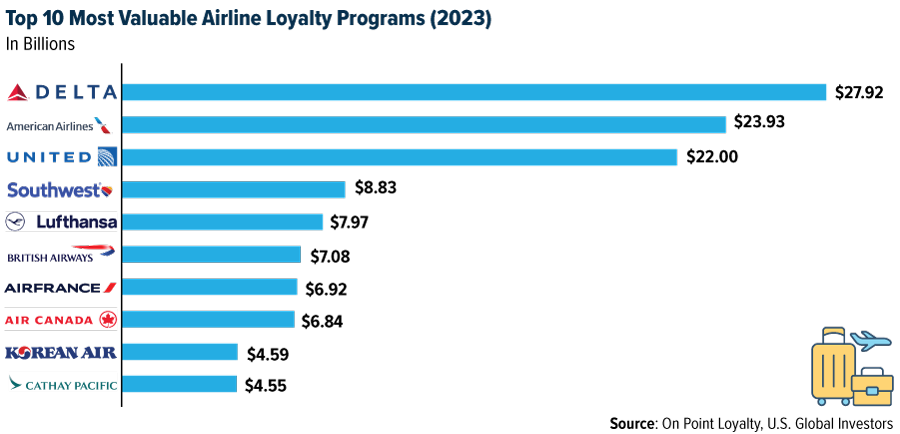

During the pandemic, when American Airlines needed to borrow money, it used its loyalty program as collateral. Lenders valued the AAdvantage program between $19.5 billion and $31.5 billion — more than the airline itself was worth.

And like Starbucks stars, airline miles are private currency that can be devalued anytime. When Delta switched from distance-based to spending-based miles in 2023, the loyalty program fundamentally changed who it rewarded. Under the old system, miles were tied to distance flown — fly from New York to London, earn miles for those 3,459 miles traveled, regardless of ticket price. Under the new system, miles are tied to dollars spent — meaning a business traveler paying $800 for that same flight earns far more than a budget traveler who paid $200. Millions of loyal customers who’d accumulated points by flying frequently — but on cheaper routes — suddenly saw their miles worth significantly less.

A 2024 Department of Transportation investigation found that airlines were systematically devaluing their points systems and raising redemption thresholds. The Consumer Financial Protection Bureau noted similar frustrations with credit card rewards programs more broadly — points losing value, arbitrary changes to redemption rules, opacity about actual worth.

You’re not earning rewards. You’re accepting payment in a depreciating private currency controlled entirely by corporations.

So every company wants to be a bank. But here’s what makes this especially dangerous: These companies are also lending to you, in increasingly predatory ways. And they’ve engineered the psychology so debt doesn’t feel like debt at all.